Newsfeed

May 15, 2026

The European Securities and Markets Authority (“ESMA”) has published its Final Report containing draft regulatory technical standards amending Commission Delegated Regulation (EU) No 149/2013 (the “Draft RTS”)1 . The Draft RTS are intended to amend and recalibrate the clearing thresholds (“CTs”) specified in Commission Delegated Regulation (EU) No 149/2013 (the “CDR”)2 to reflect and operationalise the revised framework introduced under EMIR 3.

Focus on Uncleared Exposures

EMIR 3, which entered into force on 24 December 2024, significantly revises the framework by means of which counterparties to derivative contracts assess whether they are subject to the clearing obligation.

Under the previous regime, which remains applicable at present, both financial counterparties (“FCs”) and non-financial counterparties (“NFCs”) are required to calculate their aggregate month-end average position in over-the-counter (“OTC”) derivatives over a rolling 12-month period. In line with the principle of proportionality, FCs are required to include all OTC derivatives entered into at group level, whereas NFCs are permitted to exclude hedging contracts, provided these satisfy the EMIR hedging criteria.3

The existing framework is limited to OTC derivatives, meaning that exchange-traded derivatives (“ETDs”) are excluded from the CT calculation. EMIR 3 adjusts this approach by moving away from the distinction between OTC derivatives and ETDs to a framework based primarily on the level of OTC uncleared transactions. Under the revised framework:

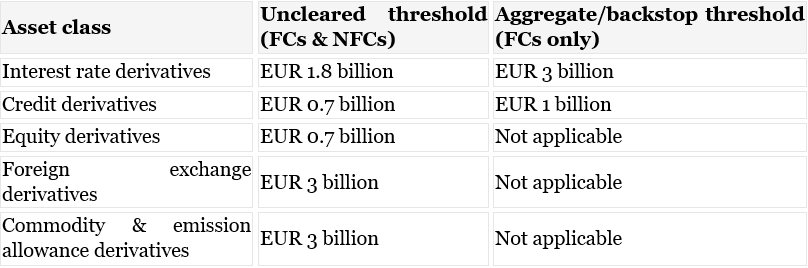

- both FCs and NFCs should calculate their uncleared OTC positions to assess whether they exceed the CTs (the ‘uncleared threshold’);

- FCs must also calculate their aggregate OTC position, including both cleared and uncleared OTC derivatives (the ‘aggregate threshold’ – also referred to as the ‘backstop threshold’).

These legislative changes necessitated further technical specification, which is provided through the Draft RTS. The Draft RTS establish that under the revised framework, NFCs must calculate thresholds based only on uncleared OTC derivatives. On the other hand, FCs must perform two calculations:

- an uncleared exposure calculation, namely the same uncleared threshold calculation carried out by NFCs; and

- an aggregate exposure calculation which takes into account cleared and uncleared derivatives in respect of the asset classes currently subject to the clearing obligation (i.e. interest rate and credit derivatives).

For FCs, a breach of either one of the uncleared threshold or the aggregate/backstop threshold will trigger the clearing obligation.

Recalibration of CT values

The CTs are expressed as gross notional amounts by asset class. The current thresholds under the CDR are as follows:

- EUR 1 billion in gross notional value for OTC credit derivative contracts;

- EUR 1 billion in gross notional value for OTC equity derivative contracts;

- EUR 3 billion in gross notional value for OTC interest rate derivative contracts;

- EUR 3 billion in gross notional value for OTC foreign exchange derivative contracts;

- EUR 3 billion in gross notional value for OTC commodity derivative contracts and other OTC derivative contracts not provided for under points (a) to (d)

While EMIR 3 invited ESMA to consider introducing more granular thresholds, for instance to include distinctions within commodity derivatives and crypto-related instruments, ESMA has elected to retain the existing five asset classes, citing operational simplicity and proportionality considerations. In relation to commodity derivatives based on crypto-related features, ESMA has elected not to introduce more granular thresholds, justifying its decision on the basis that such products would fall within the residual asset class covering OTC derivatives not captured under points (a) to (d).

While the asset class structure has been retained, ESMA has recalibrated the numerical thresholds to reflect the revised methodology as follows:

CT calculation at entity level for NFCs

Under the current regime, NFCs are required to include OTC derivatives with all other NFCs within the same group which are not hedging contracts. Under the Draft RTS, while FCs will continue to calculate positions at group level, NFCs will be required to carry out the calculation at entity level only. NFCs will also continue to benefit from the hedging exemption so hedging contracts entered into by NFCs will continue to be excluded from the CT calculation.

This shift to an entity-level calculation combined with the focus on uncleared positions will likely reduce the number of NFCs exceeding the CTs, limiting the application of the clearing obligation to NFCs.

Timeline and next steps

From a timing perspective, the Draft RTS have been submitted to the European Commission for adoption. The Commission is expected to consider endorsement within the standard three-month period, although timing remains subject to the legislative process. While no definitive timeline can be confirmed at this stage, the revised framework is generally expected to come into force in Q3 or Q4 2026, following adoption and publication of the Draft RTS in the Official Journal.

In the interim, the current CT regime will continue to apply until the Draft RTS are formally adopted and enter into force following their publication in the Official Journal. Once in force, ESMA has indicated that counterparties may apply the new calculation methodology at their usual annual assessment point to facilitate an orderly transition to the revised regime, allowing for a degree of flexibility in implementation.

The Draft RTS represent a significant step in operationalising the EMIR 3 CT framework. While the core structure of asset classes has been preserved, the shift towards an uncleared exposure-based methodology, combined with recalibrated thresholds and changes to calculation mechanics, marks a significant revision of the CT regime.

Market participants should begin assessing the potential impact of the revised thresholds on their classification and clearing obligations, in advance of the formal adoption and entry into force of the RTS. In particular, FCs should begin preparing for the introduction of the dual-test framework based on both the uncleared and aggregate threshold calculation.

1ESMA74-1049116226-944, published 25 February 2026, available here: ESMA Final Report

2Commission Delegated Regulation (EU) No 149/2013 of 19 December 2012 supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council with regard to regulatory technical standards on indirect clearing arrangements, the clearing obligation, the public register, access to a trading venue, non-financial counterparties, and risk mitigation techniques for OTC derivatives contracts not cleared by a CCP, available here: Delegated regulation – 149/2013 – EN – EUR-Lex

3In terms of EMIR, hedging contracts are contracts which are objectively measurable as reducing risks directly relating to the commercial activity or treasury financing activity of the NFC or of its group. An OTC derivative contract is considered to be objectively measurable as reducing such risks where it meets one of the following criteria: (a) it covers the risks arising from the potential change in the value of assets, services, inputs, products, commodities or liabilities that the non-financial counterparty or its group owns, produces, manufactures, processes, provides, purchases, merchandises, leases, sells or incurs or reasonably anticipates owning, producing, manufacturing, processing, providing, purchasing, merchandising, leasing, selling or incurring in the normal course of its business; (b) it covers the risks arising from the potential indirect impact on the value of assets, services, inputs, products, commodities or liabilities referred to in point (a), resulting from fluctuation of interest rates, inflation rates, foreign exchange rates or credit risk; (c) it qualifies as a hedging contract pursuant to International Financial Reporting Standards (IFRS).

Author

Related Articles

More Insights